Climate Transition Risks

How to Put the Cart before the Horse

This is a background article to the Firebreak assessment of the decade-long movement to place climate disclosure at the heart of the business management process. See Part 1 here. While focusing on how one NGO, the CDP (Climate Disclosure Project) manipulated the process for their own interests, the concept of a climate transition risk was developed in parallel to the disclosure and ESG movements. After a decade of leading the business world down a dark rabbit hole, 2024 saw a reversal of fortune for these campaign strategies (at the regulatory, business and consumer levels). This carbon disclosure series looks at the tactics these activists used and how close they came to destroying western prosperity and well-being.

There are many types of risks to be managed, from financial risks, market risks, socio-economic risks, health and environmental risks, reputational risks, political risks... It was only a matter of time, perhaps, until activists created their own type of risk: transition risks.

Last year the Firebreak argued that “transition” was the key buzzword for 2023. With climate change as the main story driving our western narrative, activists and climate campaigners speak of the need to transition away from our old practices – as part of a green transition - but what they are arguing for is a revolution in everything but name. They are targeting a post-capitalist transformation of our economy and using the manufactured threat of catastrophic climate collapse to push this revolution (transition) forward. Some examples of the urgent transitions our developed societies need to implement as soon as possible are:

Energy transition

We are told we need to move away from all forms of fossil fuels to a selection of renewable energy sources as soon as possible. Reducing CO2 emissions is the justification but when the nuclear energy option is suggested to maintain a baseload for the energy grids, activists start talking in circles. This transition is focused primarily on the goal of deindustrializing our energy supply.

Food system transition

We are told that conventional farming is destroying the soil, water, air and climate and that the only solution is a food system transition away from factory livestock farming, synthetic chemical pesticides and fertilizers. Reducing CO2 emissions is the justification but when the GM or gene edited seed option is suggested, activists start talking in circles. This transition is focused primarily on the goal of deindustrializing our food supply.

Mobility transition

We are told that the CO2 emissions from flying, driving and shipping across global markets is a major driver of climate change and that the only solution is to transition to electric vehicles, buying local and using public transportation. Reducing CO2 emissions is the justification but when the energy costs and the resources needed to be mined for this green transition are accounted for, activists start talking in circles. This transition is focused primarily on the goal of deindustrializing and deglobalizing our markets.

Economic transition

The ever-expanding markets and wider wealth divides are unsustainable and stressing the planet’s limits. A transition to a degrowth economy and a “conscious capitalism” is required to fight climate change and deliver a more just society. Reducing CO2 emissions is the justification but when degrowth causes price increases, job losses and failing services, activists start talking in circles. This transition is focused primarily on the goal of deindustrializing our economy, but is impoverishing populations.

These transitions (revolutions) are seen as urgent in order to act in the fight against climate change. There may be other reasons to argue for these transitions (increasing rates of obesity, poverty levels or traffic jams and air pollution...) but the “existential threat of climate change” became the battering ram that could best amplify the activists’ calls for transition.

There are other strategies than transitioning out of everything that can be taken (and have been taken over the last 50 years) to improve the environment and public health. Product stewardship and its strategy of continuous improvement has made industry impacts incrementally and then exponentially better. But promoting better technologies, innovations and lifestyle improvements are not enough, are not welcome and are not in line with the political objectives of the interest groups lobbying for a new realignment of the capitalist system (they call for a “just transition”).

As climate change dominates the western political narrative, climate fear is the motivation these activists need to push through their objectives. So the risk managers in the financial community, in pursuing their own interests over the last decade via their climate disclosure and ESG strategies, coined a new term to manage away any resistance from the old industrial and economic models.

Transition Risks

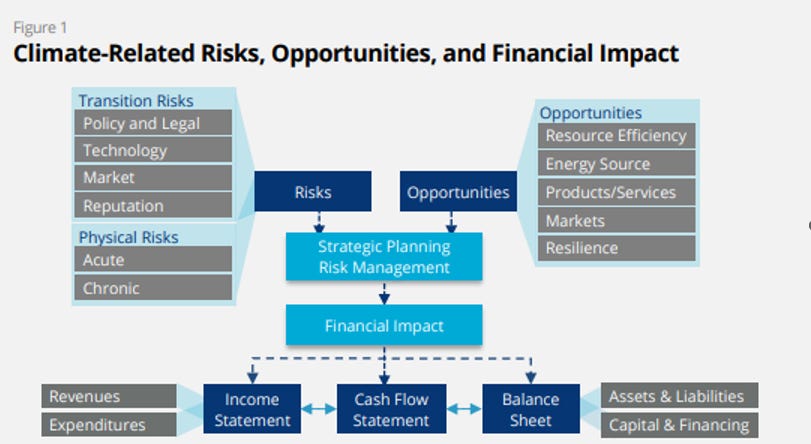

A business is not only exposed to the risks of material or physical damage from climate change, it is argued, but also business, market and reputational damage from not making the transition to green technologies. According to the activists behind this campaign, transition risks could be a far greater threat to a business than any other risks.

According to the World Resources Institute, a transition risk refers to

“the ways that reliance on fossil fuels could undermine a business as the world shifts away from them. For instance, a company that produces products such as cement or beef using carbon-intensive methods may become undesirable to consumers as preferences shift toward more climate-friendly options. This is a market risk.”

There are four key transition risks:

Policy and legal risks (should regulations restrict or ban a company’s high CO2 emitting products or if companies might face litigation threats);

Technology risks (where delays in adopting green technologies could affect new product developments or leave a company behind);

Market risks (if markets move toward green alternatives affecting supply and demand relationships); and

Reputation risks (when consumers reject higher polluting businesses in favor of more sustainable alternatives).

Companies that can manage these transition risks, it is argued, will benefit from better resource efficiency, energy use and access to renewable energy, more sustainable and low emission products, new markets and the ability to adapt to climate change and better seize opportunities.

The automotive, agricultural, chemical and energy sectors, one could argue, face the highest level of transition risks as their products or processes are regarded, by the activists, as the least ecological. The finance and investment industries are the least affected so it is little surprise that they are the key drivers behind the push for climate disclosure projects.

A good part of the research behind transition risks came from the Michael Bloomberg-led Task Force on Climate-related Financial Disclosures report from 2017, updated in 2021. Many of the actors involved in this taskforce were the main drivers behind the World Economic Forum’s movement toward leading the financial community’s climate response agenda, pushing ESG standards across all industries and envisioning a post-capitalist, degrowth economy.

They were delusional.

These transition risk architects are not very genuine in their motives. It is not that companies that don’t transition away from fossil-fuel-based practices will suffer lost market opportunities, outdated technologies and public reputation and litigious attacks, but rather, it is the risk that they will continue to do well as businesses benefitting from cheaper, abundant fossil fuels. The real transition risk is that industry won’t follow the activists down their decarbonization rabbit hole, leaving them with little else than a failed campaign and a tarnished display of virtue. It was almost an act of desperation to extort all industries to comply with their disclosure programs, albeit brilliantly executed and lobbied over a period of ten years, but ultimately failing in the last year, not on the trading floors, but at the ballot box.

Problems of Concept

The transition risk concept is not actually a risk management concept.

Risk = hazard X exposure

A car, for example, is a hazard and the risk of harm increases when I expose myself closer to traffic situations.

Risk management is the act of reducing the exposures to certain hazards to as low as reasonably achievable (or practicable)

A traffic risk manager would reduce pedestrian exposure to cars by installing zebra crossings, traffic lights or speed limits. The question for risk managers is what would be a reasonable risk reduction measure to take. Should we build a pedestrian tunnel under every intersection (regardless of the level of traffic)?

Climate change is identified as an intolerable risk, but then it is substituted in the transition risk equation by the risk of using (any type of) fossil fuels. The transition risk concept identifies market demands for decarbonization as the hazard and the failure to act (by still using fossil fuels and not adopting green technologies) as a company’s exposure to the hazard. Put positively, a company can reduce exposure to risks by transitioning to renewables in place of fossil fuels. But these decarbonization options are potential solutions that carry with them a high degree of uncertainty (unlike physical risks that can be managed by a large number of climate mitigating measures to reduce exposure). If you can’t measure it, you can’t manage it, and with the transition to renewables and the carbon carousel game, there is no serious or accurate tool for measurement.

The creators of the various climate disclosure projects assume that disclosing CO2 emissions will allow businesses to identify transition risks (and assumedly, reduce exposure to them by then adopting green technological alternatives). But disclosure is not a risk-reduction measure, it is a tool for examining where the risk may lie (a risk assessment). It is only one little part of the process.

Risk assessments need to factor in all potential risks and all scenarios while the carbon disclosure strategy attempts to prioritize this (minor) element of a risk assessment. For people like Michael Bloomberg, I suppose, if the only tool you have is a hammer, everything looks like a nail, but in the risk management world, things are a little more complicated.

Worse, adopting the activists’ exposure reduction requirements may not reduce overall market risks. Consumers may not be willing to pay so much more for energy, buy electric vehicles with low resale values or eat food that is visually unappealing or lacking proper protective packaging. These are more serious business risks than the threat of implementing a more measured (more reasonable) green transition than what these impatient activists are demanding. These are problems of execution.

Problems of Execution

The problem of making climate change a certain hazard (and transition to green technologies the only reasonable means to reduce exposure to this hazard) is that the transition risk advocates created some very unreasonable management solutions.

Green, renewable energy was insufficient, intermittent and expensive (and, often, not very green)

Organic food was insufficient, and expensive (and, often, not very green)

Electric vehicles were expensive and not technologically mature (and, often, not very green)

Ultimately the problem is that you cannot force through transitions if the technology and the consumers are not ready. What the transition risk activists did was go straight to the financial markets and fund managers to force industries to comply with their transition demands before the technologies and the markets were ready. It created unrealistic artificial demands on supply chains where down-market brands were putting unrealistic decarbonization conditions on their producers.

The most ridiculous example of this unrealistic supply chain forcing is when manufacturers of French fries and chips demanded that potato farmers grow via no-till practices in order to improve their own CO2 emission / ESG scorecards. Someone should tell these carbon bean counters that potatoes grow in the ground.

ESG was nothing more than fund managers extorting industry to relent to their CO2 disclosure and reduction demands (otherwise their shares would be delisted from their ETFs). The carbon disclosure projects set up by NGOs like CDP were an integral part of this movement to push certain industries out of business.

The activists assumed that consumers would be ready and willing to make sacrifices, that companies would be ready and willing to impose stifling conditions on their markets and that the climate fear rhetoric could remain impactful, regardless of the measures imposed on consumers.

The electoral decimation of political parties supporting these green transition policies during the 2024 elections should be enough indication that there are other risks far greater than their artificially imposed transition risks. Politicians, business leaders and academics quickly abandoned the green transition rhetoric when it became evident that consumers (voters) had had enough and were no longer (literally) buying it.

Within the Context of the Climate Disclosure Campaign

This article on the concept of transition risks stemmed from my research into the climate disclosure campaigns and the decade-long dominance of NGOs like CDP (the Climate Disclosure Project). The Task Force on Climate-related Financial Disclosures articulated many of the movement’s objectives, swiftly implemented by opportunists in the financial services sector. A transition risk was a clever tool created to force industries into complying with their interests and opportunities.

But a large amount of these investment funds are dumb money managed by lazy analysts (or bots). As many ESG funds were not much different from traditional ETFs or their results were markedly less impressive, investors were no longer sold by the “opportunity” or the “virtue” and industries were not as compelled to comply. Forcing companies to pay an NGO to disclose their CO2 emissions or be blacklisted by a financial community that has discovered virtue and purpose no longer carried very much teeth.

It can be argued that the ESG downfall, apart from being built on baseless fears and unreasonable solutions, had to do with a weak understanding of actual risk management. You would think that these highly-paid investment fund managers and their financial institutions would be able to tell the difference between risk management and risk assessment. But it is not the first time these chartists have been seen to be risk illiterate. The financial industry is driven to a large part by opportunity and greed, and, as the 2008 financial crash attests, their motives have very little to do with risk-reduction measures. These (former) ESG fund managers should all be fired (or set on fire), but I suspect they have already piled into the next big pot of gold.

I hear private finance is the place to be.